Heroin overdose is my retirement plan at 70-80 depending on my health.

pretty good here in Australia, we have superannuation which is basically like a forced savings account so when you retire you get a nice little present

I heard you can pick and choose where your supers go, so you’d be able to actively ‘vote with your wallet’ by pulling it out of companies you didnt like, is that actually a thing or am I misremembering a jordies vid segment from years back?

sure is :)

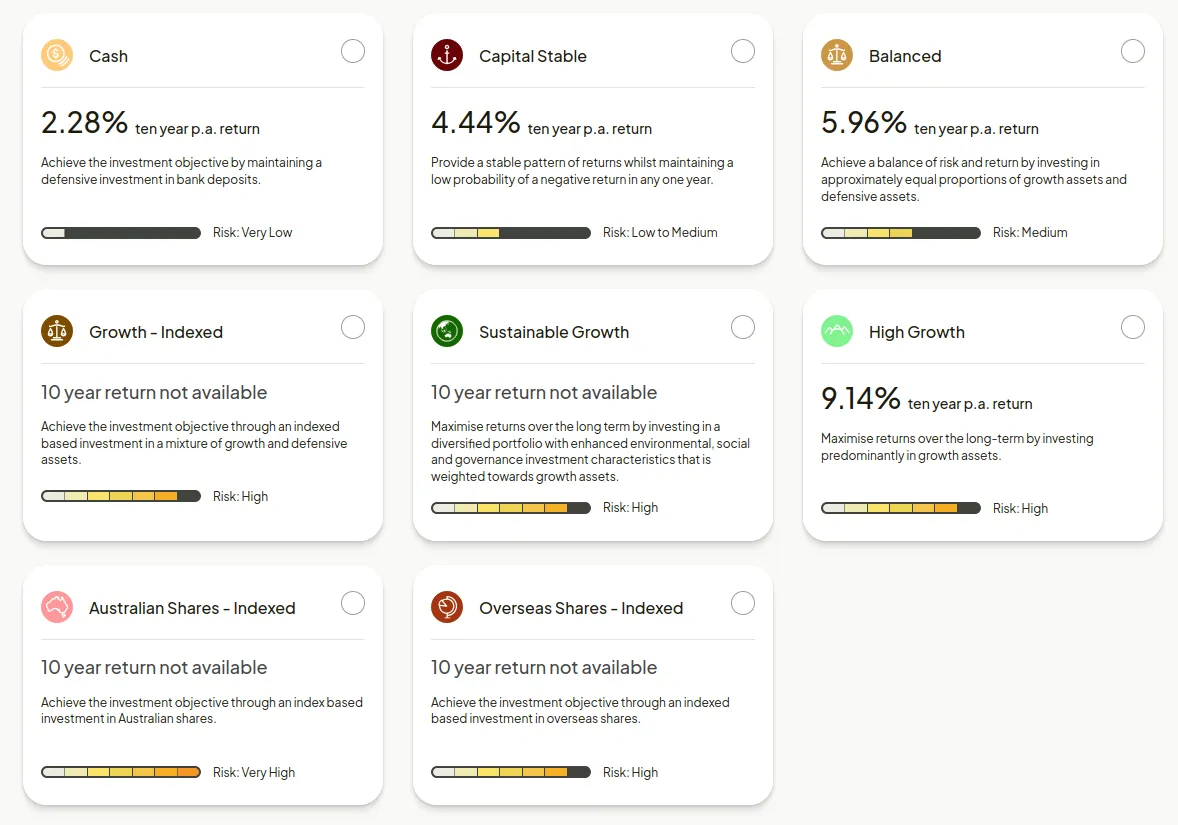

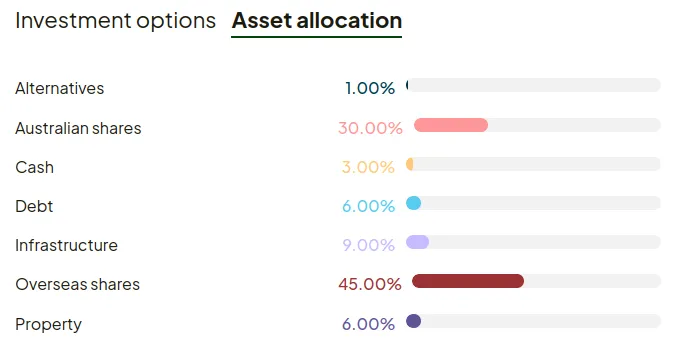

I’m with Rest since they were recommended to me working at my first job and they seem pretty competitive and then yeah it’s basically just the same as picking ETF’s, where you go based on your risk levels you want to take, if you’re young pick the riskiest, if you’re older and about to retire pick the safest

I am 100% in Sustainable Growth ofc

Maximise returns over the long term by investing in a diversified portfolio with enhanced environmental, social and governance investment characteristics that is weighted towards growth assets.

https://rest.com.au/investments/options/compare#super

You can also self manage your own super but I think only around 5% of people do that

Hell yeah go help that state down south smash more renewable records and maybe the rest of your parliament will go ‘hangabout ,we’ve got just as much sun as them, why are some of them being paid to use power during offpeak hours?’

Except everyone’s looking for ways to spend it science covid.

There are ads on YouTube now for Self Managed Super Funds that allow you to

gambleinvest in stocks, ETF’s & I dread to think what. Prediction markets?Edit: super is still a pretty good idea.

For once the UK system looks ok in the world; our ’forced savings’ of ‘national insurance’ paid as a tax style deduction on wages can’t be touched till state retirement age, so you’ll get it when you retire and it’s paid monthly not a block. It used to be set at 65, now it’s on a rising rate for people retiring in the next years. I’m in a group that will need to be 67. It’ll be really basic, and a private pension is expected in addition if you want to have a nice retirement rather than just managing.

Think of super as the same, but you employer matches your forced contributions and, up to a limit, voluntary ones.

Better then, for us to get an employer contribution, at least a visible one as they pay tax on employment as well, you go to a private scheme in addition to the state one, but then that’s where some people may not have that, and be reliant on state only.

Well it’s either you gamble it or you pay them to do it for you. If you just go s&p500 and vanguard world anyway might as well do it yourself and save some fees.

Industry super funds usually have super low fees and a fairly conservative investment strategy. Theres AUD$4.5trillion invested between them all

The same thing that happens every generation to the god-awful number of people who never had hope of retiring to begin with.

30 years? It’s happening right now!

no retirement savings, but at least they own the place they live

god help the next generation

While we need* property taxes, it absolute hammers old people in some places.

Cheaper than renting still, but on a fixed income it hurts, and especially lately there have been very high tax increases due to inflation. But then the social security increases are comparatively small.

I know quite a few old people struggling and it seems like their plan was to own their home. But that turned out more expensive than expected with maintenance and taxes. Which has just led to cyclical reverse mortgages. So the banks win in the end and ensure no transfer of wealth

*It’s necessary under the current system to fund services, but if we took it from elsewhere (like the ICE of military budgets) we could greatly reduce that tax.

Easy, property tax deduction on first 50% median price and then ramp up the tax rate above 200% median and above.

A refund based on assessed median home value would tend to penalize new home buyers over existing home owners, even if the existing home owner has a house that would sell for higher. Property tax assessments rarely keep up with home valuation.

I don’t quite get what you’re saying. If median home is 300k and your home is 350k assessed, then you pay property tax on 200k. 500k? Then 350k. Up to 600k where it would phase out and increase instead. I don’t see how that penalizes new home or first time home buyers. It subsidizes new homes with low assessment, starter homes, and downsized homes for the elderly. It penalizes homes worth more than 2x median.

Yes once a new home is fully assessed it could cost more potentially than an older home, but a good property formula solves for much of that. Usually it’s based on square foot and materials, not age.

In most places in the US, the assessed value of homes that have been owned for more than a decade is significantly less than the market value of a home.

The property tax burden therefore falls more on new home buyers rather than existing home owners. Eliminating the tax on the first portion of assessed value would make this existing imbalance worse, especially if the same amount of tax needed to be raised.

It’s a tricky problem.

Even if you own a house, there are still plenty of expenses, like bills, property tax, groceries, healthcare ('Murica), and the occasional small luxury to stay sane.

Modern day Social Security isn’t even going to cover half of that.

My boomer mom inherited a house that was paid off and almost immediately did a reverse mortgage on it. 😔

To make necessary repairs to the house… right?..

Um… no.

It’s the normalisation process.

Same thing that happens to the people who have no savings now when they reach state retirement age. They simply can’t afford to, and have to continue working.

Unfortunately retirement is as much a financial state as it is an age.

Is this really you irl?

Retirement is not an age, it’s a financial status.

it’s a mindset

You make it sound like it’s supposed to be that way?

Nah, that’s all you.

how?

when most people live paycheck to paycheck, and their biggest luxury is a bobba tea once a month, how the fuck can you do anything about retirement?

the system is set up to maximize human suffering for profit.

It simply stated the reality that retirement comes from having resource access without requiring employment. That’s what it is. Hearing judgement about what should be is you adding it.

I didn’t read it that way. It’s just a fact. If you had enough money saved/invested, you could reasonably retire today. If you don’t have anything saved, you can’t afford to retire at any age.

As the OP shows, even the pension system in the UK (or social security in the US) amounts to little more than a sick joke in comparison to the actual cost of living.

I know I’m not saying anything new, I’m just rephrasing the GP’s point in a particularly verbose way.

If you don’t have anything saved, you can’t afford to retire at any age.

But it’s not supposed to be that way.

even the pension system in the UK (or social security in the US) amounts to little more than a sick joke

BUT IT’S NOT SUPPOSED TO BE THAT WAY!

People usually don’t retire because they can but because they have to. Because they can’t work anymore. Framing it like retirement based on savings only is just an unchangeable fact of nature is just wrong.

But it’s not supposed to be that way.

You’re too focused on this, IMO. I can’t fix the injustice here all by my lonesome. What I can do is live beneath my means, save up the extra (and I’m fortunate to have extra after paying for the bare minimum), and have something beyond social security for my own retirement. That’s all any individual can do.

In a group? In the US, you can vote according to who you think will run Social Security better. But in practical terms, that’s a choice between bad and worse. I don’t like it any more than you do, but I don’t see a realistic alternative in the near future.

In the UK (or other countries)? Someone else will have to weigh in there.

This still refers to this shitty comment:

Retirement is not an age, it’s a financial status.

I’m not saying you should overthrow the system tomorrow, but those seemingly witty comments that just normalise how messed up the system is just don’t help.

Retirement is not a financial status. Stupid teenagers that listen to right wing podcasts may think such a remark seems smart, but it is stupid and wrong. Retirement is a necessity that stems directly from the fact that people just can’t work as well at 90 as they can at 35. It’s not a hard concept to grasp and the fact that society makes it hard to stop working after people worked a lifetime but can’t go on anymore isn’t some wisdom to understand, it’s just a neocon’s wet dream and should be described and treated as such.

It would be nice if everyone could be afforded some kind of retirement when they got older. You are correct, in general a 90 year old will be nowhere near productive as a 35 year old. But it would also be nice if people working full time didn’t need food stamps, and if the tax rates were higher, and a whole bunch of other stuff. But that’s not the world we’re living in.

I have to agree with OP here, right now it IS a financial status. It’s a luxury only afforded to those who have the wealth. The whole idea of “retirement” is fairly new. Even 100 years ago a 90 year old might move in with their kids, provide childcare for the grandkids, help out around the house, etc.

Just to reiterate I am on your side, retirement SHOULD be something afforded to everyone. That’s just not the world we’re living in.

Hopefully we’ll vote better.

Well let’s not presume to know, instead ask yourself which two groups of society won’t care at all:

Rich people won’t care because their children will have inherited enough to be set for retirement.

The children of rich people, because their parents were able to save for retirement.

Well and those who earn a decent living because their parents were rich and able to provide a decent education which allows staying above the current job market Like me.

I won’t be able to afford a house ever. But if I prioritize earning over my health its gonna be enough. But I already have to choose between providing a decent education for my three children or retire at more than the absolute minimum.

A massacre

Soo prime for revolution

That’s assuming that we’re still here in 30 years, and not living is post apocalyptic wasteland

Climate wars are here, we just don’t recognize them as such.

America is already blockading Cuba and ran a hostile takeover of Venezuela, america also destabilised Iran in the 50s or thereabouts was because they wanted to privatise and keep their own oil, so they did a bit of their ‘regime change’ and suddenly the heavily oppressive highly religious leader is happy to sell oil to big america.

We’ve been in the resource wars for a long while.

Go back just a bit further to when Britain invaded Iran for full accuracy.

I won’t claim the empire was ever a good thing but that was less resources and more straight up territory landgrabbing touted as ‘spreading civilisation to the colonies’ (where do you think america got the idea for ‘spreading democracy’-learned it right from papa britain)

Britain literally invaded Iran during WWII and found every reason to stay (well oil but ya know)

Hahahahahahahahahaha

Do you think we’re actually going to survive the next 30 years?

We are putting as much energy as 13 fatman bombs into the planet’s environment EVERY SECOND.

The only time in the past 25 years we weren’t putting energy into the system, and the earth could radiate out more energy than we put into it, was summer 2002.

Now I’m curious, what happened in summer 2002?

Nothing, but it was the first period in the last 25 years.

Big dip in the graph

Potentially a lack of air traffic, or a knock on effect of an economic crisis lowering the level of pollution,

And a bunch of people were scared to fly because of 9/11

FUCK

I know this sort of thing usually happens in a form such that the OP sees the meme already edited on another site where censorship is a concern and then shares the image without modification because finding the original is a pain, and I don’t blame the OP for it, but man is it an annoying cultural phenomenon.

I’m 50; when I started my career pretty much everyone a little older than me had pensions and I arrived right as the pensions were being phased out. It was a running joke when they would talk about pensions and I would say “what’s a pension?”

So my age group will be retiring in 15 years, not 30 years. Almost everyone I know my age has a meager 401k and nothing else.

The streets are going to be flooded with people too old to work and no retirement income in much less than 30 years…

56 here, I’m in the UK. I have 4 separate ‘private pensions’, from the four different companies I’ve worked for, adding up to fuck all. Basically I’m going to have to work until I’m 67 in order to collect my state pension of £1,049.22 a month. This will allow me to survive on cold baked beans out of a tin, before I freeze to death because I can’t afford to turn on the heating.

Why do those private pensions not amount to anything?

I didn’t get the benefit of a final salary pension. I have also not worked long enough at any particular company to really benefit from a big pot. The longest I’ve worked for one company is ten years, I think the company was paying in as little as possible. When I looked at a forecast for the pay out from that one, it was about £100 a month.

You should consolidate those 4 pensions into one pot and take more control of it. There’s an extremely high chance that the employer provided pension is performing poorly and not growing as fast as it could be. They pick the lowest risk by default so growth is massively stunted.

It’s pretty easy to open an account on something like vanguard and transfer those pensions in, you can then have control over how that money is invested - usually they make you pick a “risk factor” where highest risk has highest potential growth and lowest has lowest potential for crashing, but the TL;DR is over a 15 year period even if there’s a crash you’ll come out on top because it averages out.

Essentially what I’m saying is pool your pensions together and pick the highest risk factor for the next 8-10 years, it’s a bit of a gamble but it’s a better chance of that pot growing into something actually useful than you have right now.

Because a lot of pension plans are very disappointing. They for example offer a ‘guaranteed’ minimum intrest of up to 2 % per year, but don’t forget the ‘management costs’ they charge. That’s very very low compared to regular inflation. Pension funds exist to make pension fund managers, traders and banks rich (now, not later) and so that the government can point at them and say “it was your own responsibility!” instead of offering ALL weak and old people enough to cover basic needs. And that’s to “motivate” as many people as possible to work as much as possible. If relatively young right now: you’re probably better off putting money away in time deposits with higher guaranteed intrest than putting it in pension funds. Or ETF/random stock picking for those who feel lucky. The state subsidies to choose pension fund instead of time deposit or direct market investments is in many cases also misleading: you get tax cuts when depositing into the pension funds, but you get taxed when you get paid out at pension age. All differs a lot in different countries, but the core of it is pretty similar all over I think.

I hope they’re at least Branston

The pensions in the US for the generation before me were “Defined Benefit” pensions. What that meant typically is that if you worked X number of years you could retire with Y percentage of your salary. Both my grandfather and father retired that way.

Private corporations all switched to 401ks and colluded with all kinds of propagandists to convince the workers that they would be better at investing their own retirement money themselves, ya know, because they were all savvy investors.

Just based on the Google search I just did 15 seconds ago a “private pension” in the UK is the same tax-sheltered retirement savings account that gets funneled to the markets as a 401k is here in The States.

So yup, you got screwed too.

“You guys are getting 401ks?”

{kind=link}